Bitcoin’s drop over the past three months has revived a familiar line of commentary about an oncoming crypto winter. The price is down roughly 18% over the period, and some commentators have pointed to weakness in crypto equities as evidence that the broader market is breaking down.

One of the steepest moves came from American Bitcoin Corp., which plunged about 40% on Tuesday thanks to unusually heavy volume. The decline spilled briefly into Hut 8, which owns a majority stake in the company. Other Trump-linked digital assets have also fallen sharply, feeding a broader narrative that the sector is rolling into another prolonged downturn.

Market structure data, however, does not support that view.

According to a new report from Glassnode and Fasanara Digital, bitcoin has attracted more than $732 billion in net new capital since the 2022 cycle low.

The report notes that this single cycle pulled in more inflows than all previous bitcoin cycles combined and pushed realized cap to roughly $1.1T while spot price rose from $16,000 to about $126,000 at the peak. Realized cap is a measure of true invested capital and is typically one of the first indicators to contract during real winters. That is not happening.

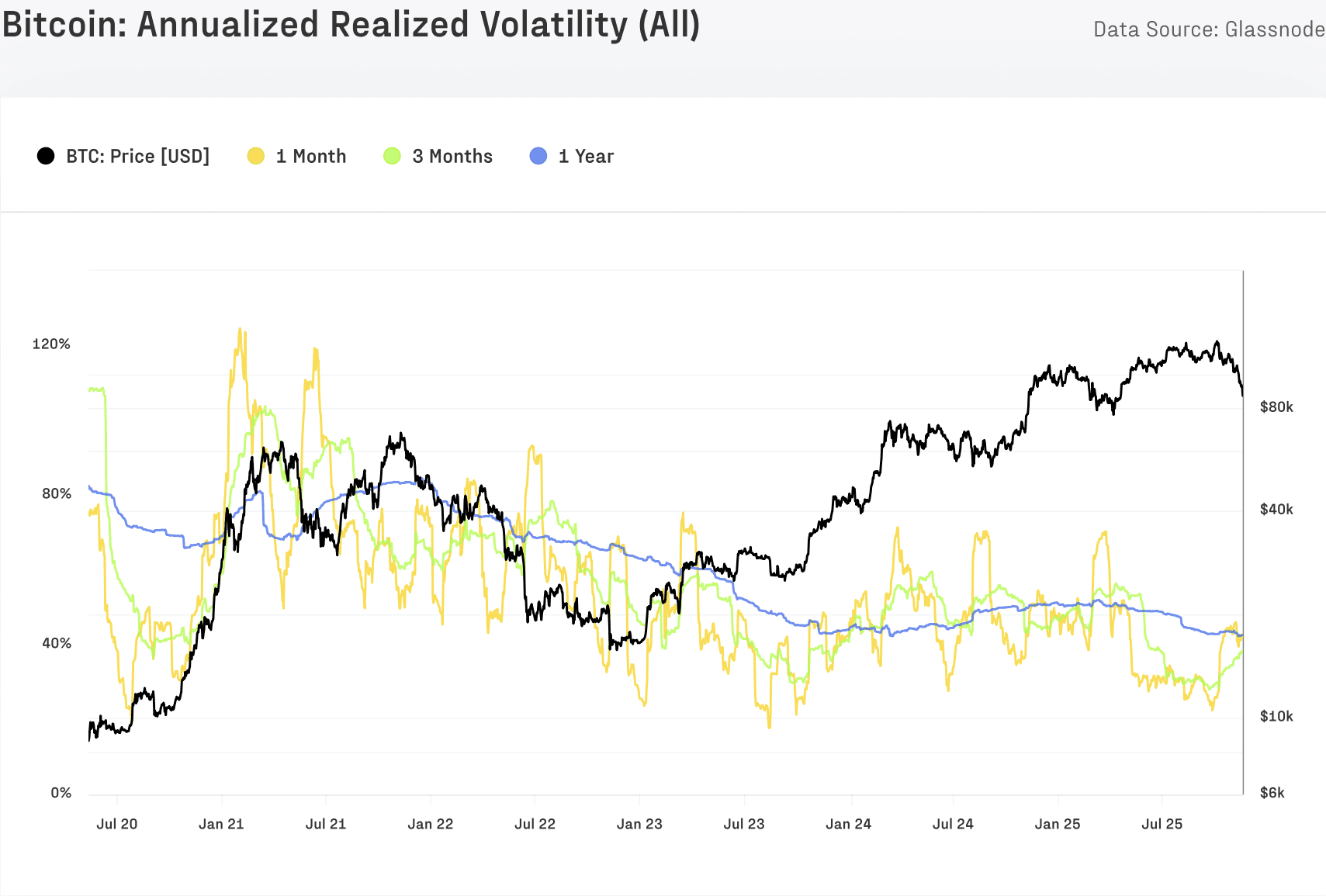

Volatility tells a similar story.

The report shows BTC’s one-year realized volatility falling from 84% to about 43%, a decline associated with deeper liquidity, larger ETF participation, and more cash-margined derivatives.

Winters begin when volatility rises, and liquidity evaporates, not when volatility is cut nearly in half. What that’s historically true, this cycle is marked by growing popularity of call overwriting strategies in BTC and IBIT options. These strategies have dampened volatility this cycle, invalidating previous spot-vol relationships.

The report argues that ETF activity also contradicts the idea of a cycle top. The report shows that spot ETFs hold about 1.36M BTC, roughly 6.9% of the circulating supply, and have contributed about 5.2% of net inflows since launch. ETF flows tend to turn negative and stay negative during real winters, especially when long-term holders reduce exposure at the same time. Neither condition is present today.

Sector-wide miner performance also diverges from winter patterns. The CoinShares Bitcoin Mining ETF (WGMI) is up more than 35% over the same three-month period in which BTC is down. In prior winters, miners were among the first to collapse as hashprice deteriorated. The current divergence shows that miner weakness is not broad-based and that company-specific issues, such as the American Bitcoin selloff, are not representative of the sector.

The drawdown itself fits historical mid-cycle behavior rather than a full reversal, Glassnode writes.

Bitcoin posted similar drops in 2017, 2020, and 2023 during periods of leverage reduction or macro tightening before continuing higher. The October 2025 deleveraging event cited in the Glassnode and Fasanara report matches this pattern. Open interest fell sharply in hours while spot liquidity absorbed billions of dollars in forced selling. Events like this tend to reset positioning, not end cycles.

Bitcoin also remains much closer to its yearly high near $124,000 than its yearly low around $76,000. In every past winter, the market gravitated toward the bottom of the range and stayed there as realized losses accumulated and long-term holders shifted their behavior. The present setup does not resemble that environment.

Short-term volatility in individual equities can create dramatic headlines, but the structural indicators that define market cycles tell a different story.

Glassnote points out that record realized cap, declining volatility, and persistent ETF demand point to consolidation after a historic inflow cycle.

To conclude, the present market dynamics aren’t something you’d see at the start of a crypto winter.